SMM News on May 28:

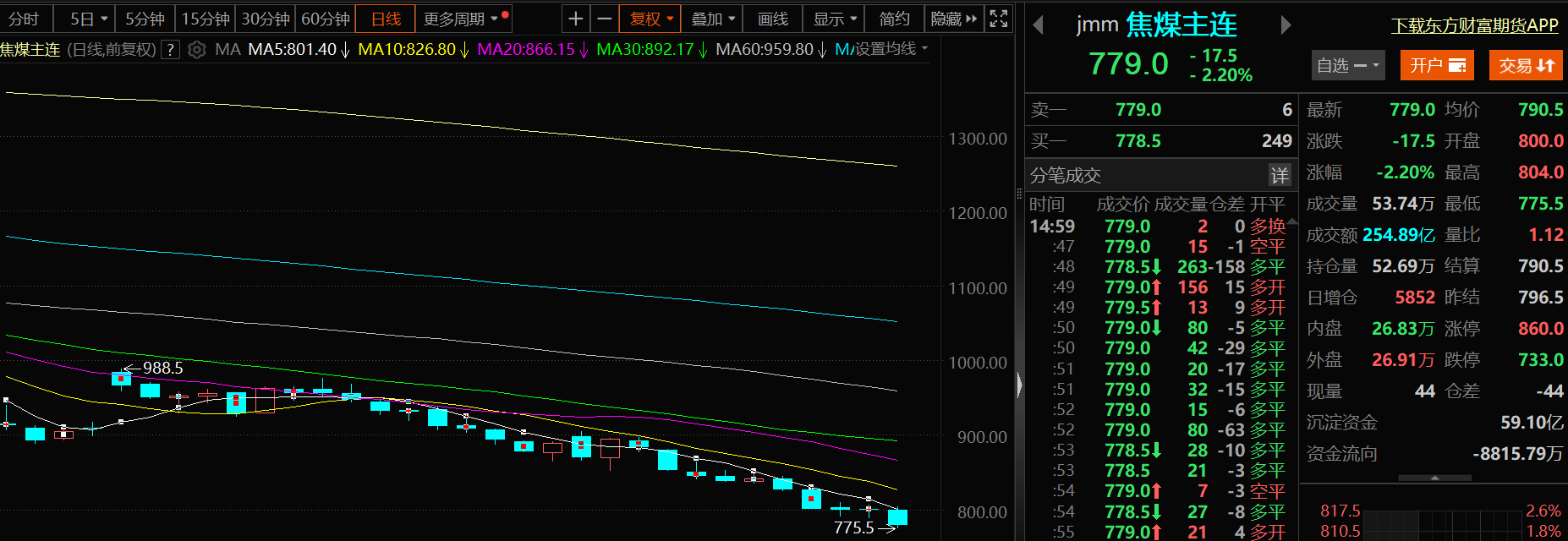

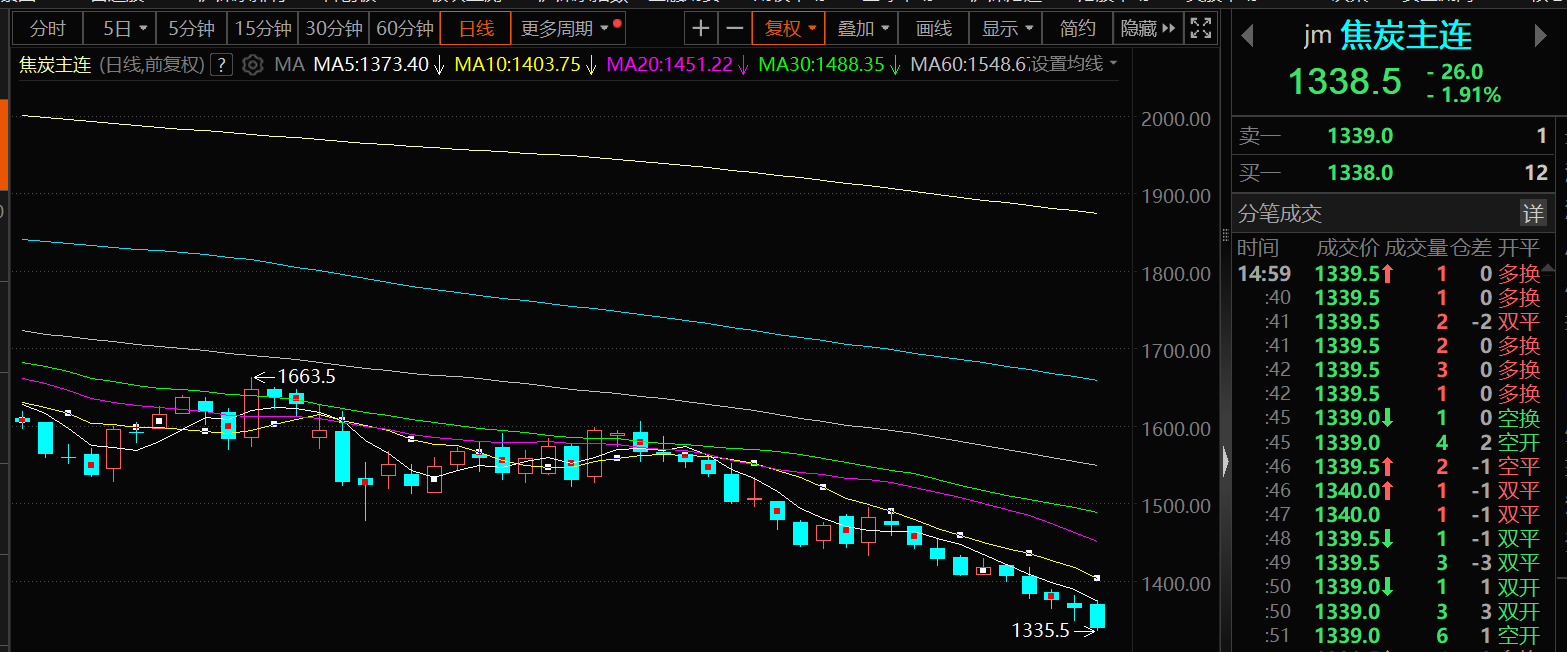

Coal mines are generally operating normally, with production cuts at individual coal mining enterprises failing to alter the loose supply situation of raw materials. The second round of coke price reduction proposals has also weakened market confidence. Recently, some steel mills have reported overall losses in profits and plan to formulate maintenance plans after the Dragon Boat Festival. Pig iron production continues to decline, putting pressure on coke prices. Pressures on both the supply and demand sides have led to declines in coking coal and coke futures over nine trading days. As of the daytime market close on May 28, coking coal fell by 2.2%, hitting a low of 775.5 yuan/mt during the session, the lowest since August 2016. Coke fell by 1.91%, reaching a low of 1,335.5 yuan/mt during the session, the lowest since October 2016.

》Click to view SMM Futures Data Dashboard

Fundamentals

Coking coal and clean coal production rise in tandem; coking enterprises' coking coal inventory may continue to accumulate

Production: According to data from the National Bureau of Statistics (NBS), raw coal production has maintained stable growth. In April, the raw coal output of industrial enterprises above designated size was 390 million mt, up 3.8% YoY, with the growth rate slowing by 5.8 percentage points from March. The daily average production was 12.98 million mt. From January to April, China's raw coal output of industrial enterprises above designated size was 1.58 billion mt, up 6.6% YoY, with coking coal and clean coal production also rising in tandem.

Imports: According to data from the General Administration of Customs, in April 2025, China imported 37.825 million mt of coal and lignite, down 16.4% from April 2024. From January to April 2025, cumulative imports reached 152.671 million mt, down 5.3% from the same period in 2024. It is worth noting that the decline in coal and lignite imports was mainly concentrated in April. From January to March 2025, cumulative imports were 114.846 million mt, down 0.9% from the same period in 2024.From January to April, China's cumulative imports of coking coal and bituminous coal were 36.33 million mt, down 3.38% YoY.

Inventory: Last week, coking enterprises' coke inventory was 348,000 mt, up 39,000 mt WoW, or 12.6%. Steel mills' coke inventory was 2.636 million mt, down 39,000 mt WoW, or 1.5%. Port coke inventory was 1.47 million mt, down 10,000 mt WoW, or 0.7%. Coking enterprises' coking coal inventory was 2.576 million mt, down 52,000 mt WoW, or 2.0%. Last week, the operating rate of coking enterprises remained stable, but their coke inventory accumulated slightly, increasing sales pressure. On the raw material side, despite coal mines continuing to offer price concessions to improve coking enterprises' profits, coking enterprises' coking coal inventory remains high, posing supply pressure. For steel mills, most currently have medium-to-high coke inventory levels, resulting in low enthusiasm for coke procurement and a gradually increasing desire to bargain down prices. Considering the operating rates of steel mills, coking enterprises, and the upstream and downstream industries, it is expected that the coke inventory at steel mills may decrease further this week. In terms of raw materials, coking enterprises have moderate profits but face difficulties in shipping their products. The market sentiment is weak, and the demand from steel mills has declined. It is anticipated that the coking coal inventory at coking enterprises may continue to accumulate this week. For steel mills, their profit margins have narrowed, and their operating rates have decreased slightly. The market sentiment is weak, and it is expected that the coke inventory at steel mills may decrease somewhat this week. Regarding port inventory, due to the poor shipping of coking enterprises and the intensified supply-demand imbalance in the market, it is expected that the coke inventory at ports may increase slightly this week.

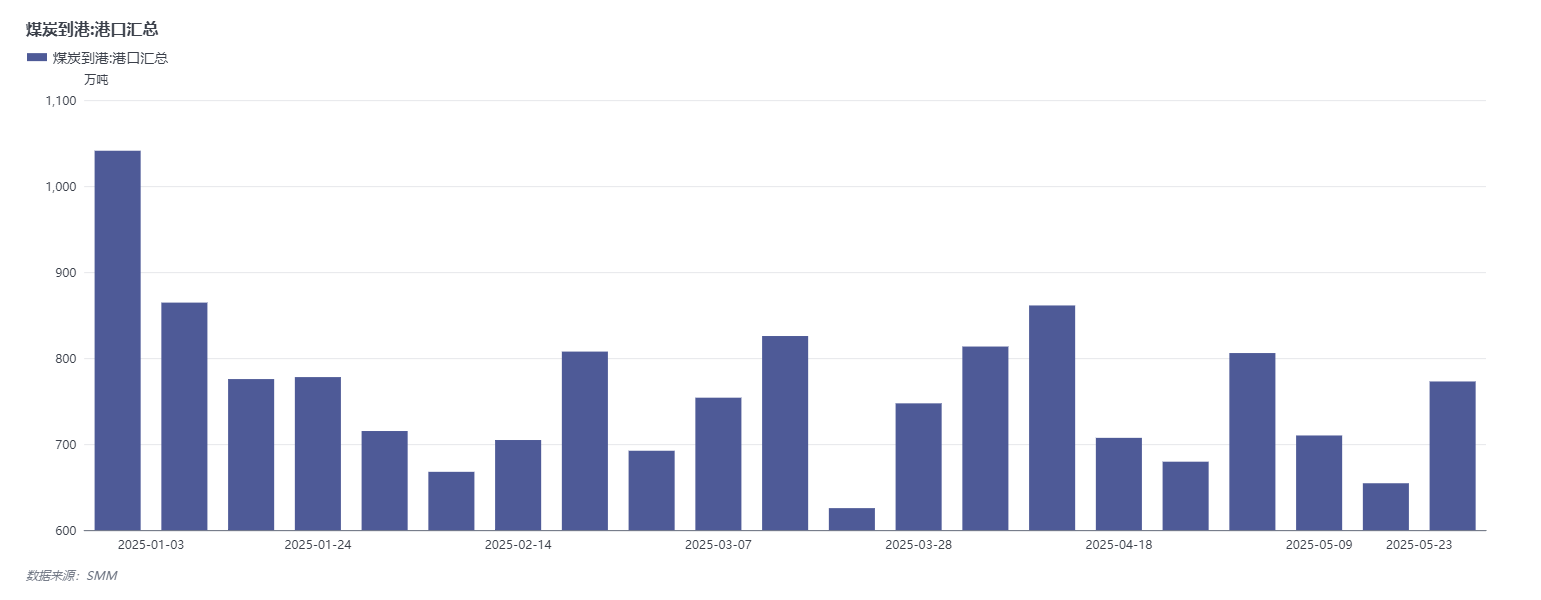

Last week, coking coal arrivals at ports increased by 900,600 mt WoW.

》Click to view the SMM Metal Industry Chain Database

In terms of arrival data, according to SMM tracking, the total coal arrivals at ports last week (May 19-23) were 7.7286 million mt, up 1.1835 million mt WoW. By type, coking coal arrivals were 2.5264 million mt, up 900,600 mt WoW; coke arrivals were 0 mt, down 4,400 mt WoW.

In terms of port departures: According to SMM tracking, the total coal port departures last week (May 19-23) were 27.0952 million mt, down 411,100 mt WoW. By type, coking coal port departures were 11.5623 million mt, up 343,600 mt WoW; coke port departures were 245,900 mt, down 36,400 mt WoW.

Spot market: The second round of coke price cuts was implemented, and market sentiment weakened further.

Spot market: On May 28, the price of low-sulphur coking coal in Linfen was 1,230 yuan/mt. The price of low-sulphur coking coal in Tangshan was 1,280 yuan/mt. The nationwide average price of first-grade metallurgical coke (dry quenching) was 1,625 yuan/mt. The nationwide average price of quasi-first-grade metallurgical coke (dry quenching) was 1,485 yuan/mt. The nationwide average price of first-grade metallurgical coke (wet quenching) was 1,290 yuan/mt. The nationwide average price of quasi-first-grade metallurgical coke (wet quenching) was 1,200 yuan/mt. According to SMM, in the coking coal market, coal mines are currently operating normally, with a few reducing production slightly. However, this is unlikely to change the loose supply situation. Downstream buyers are hesitant, and after the price decline, order signing at coal mines remains unoptimistic, leading to an accumulation of coking coal inventory. With the implementation of the second round of coke price cuts, market sentiment has weakened further, and coking coal prices may continue to face downward pressure this week. In the coke market, in terms of supply, coking enterprises have moderate profits and stable production, but face certain obstacles in shipping their products, leading to a looser coke supply. In terms of demand, south China has entered the rainy season, with frequent high-temperature and rainy weather, resulting in a seasonal decrease in steel demand. Pig iron production has peaked and pulled back. Additionally, the coke inventory at most steel mills is at a medium to high level, weakening the rigid demand for coke. In summary, steel mills have a strong desire to drive down coke prices. With the implementation of the second round of coke price cuts, market confidence has weakened further, and the coke market may continue to be in the doldrums this week.

Institutional Perspectives

Yide Futures Analysis: Pig iron production has recently peaked and is now pulling back. Attention should be paid to the pace of its decline in the future. The production of coking coal mines has decreased, mainly due to mine maintenance and tightened safety inspections in some regions, although the impact is expected to be relatively short-lived. Currently, the auction failure rate of coking coal remains high, with prices continuing to decline. The purchase willingness of downstream buyers is low, leading to a significant rebound in coal mine inventories and intensified sales pressure. The coke market is experiencing strong market pessimism, with a second round of price cuts imminent. Along with the peak and subsequent pullback in pig iron production, coke prices may face further downward pressure in the future. Overall, there has been no substantive change in the fundamentals of coking coal and coke. The loose supply situation for coking coal throughout the year is unlikely to change. Currently, the prices of coking coal and coke are still in a downward trend, with no signs of a bottom yet. The futures market is likely to remain in the doldrums.

Industrial Futures Research Report: Coking Coal: The supply of raw coal remains loose. Production at major mines in the producing areas has not tightened, and imported resources are also abundant. However, the continuous decline in spot coke prices has compressed coking profits, leading to low willingness among steel and coking enterprises to restock raw materials. Pithead transaction conditions are poor, with the auction failure rate remaining at a relatively high level. The inventory buildup pressure at the mine end continues unabated, and the fundamentals remain bearish for coal prices. Coke: With the decline in steel prices and the strengthening of expectations for the traditional off-season, the daily production of pig iron is likely to fall back from highs. The rigid demand support for coke entering the furnace is weakening, and there are more instances of downstream enterprises controlling arrivals. Raw material inventories continue to operate at low levels. Major steel enterprises in Hebei have lowered their coke purchase prices by 50-55 yuan/mt. The second round of price cuts is expected to be implemented this week, and futures prices are likely to continue their weak trend.

SDIC Futures: Coke: Prices have slightly rebounded after hitting bottom. Part of the second round of price cuts has been implemented. Pig iron production continues to drop back slightly. The first round of coking price cuts has been fully implemented, but profits still exist, so the daily production of coking remains at a relatively high level for the year. The overall inventory of coke has slightly increased, with no purchasing actions from traders. Overall, the supply side of carbon elements remains relatively abundant, and downstream pig iron production continues to drop back slightly. The sustainability of further negative feedback is being observed. The coke futures market is basically on par with parity, and it is not advisable to be overly bearish in the future, considering the sentiment in the steel market. Coking Coal: Prices have slightly rebounded after hitting bottom. The production of coking coal mines remains at a relatively high level, with individual mines taking production cut actions. The number of halted mines has increased by 2 to 18. The spot auction market has significantly weakened, with transaction prices continuing to decline. Terminal inventories continue to decrease slightly. The total inventory of coking coal has increased slightly on a MoM basis, and the inventory pressure at the production end continues to accumulate rapidly. Overall, the supply side of carbon elements remains relatively abundant, and downstream pig iron production continues to drop back slightly. The sustainability of further negative feedback is being observed. Coking coal maintains a significant discount, and it is not advisable to be overly bearish in the future, considering the sentiment in the steel market.

Zhengxin Futures pointed out: The second round of price cuts for spot coke has commenced, with coking coal and coke continuing to be in the doldrums. On the coke front, due to the concessions from raw coal, coking enterprises are maintaining moderate profitability, with operating rates remaining high and stable. On the demand side, the decline in pig iron production accelerated last week, indicating the initial signs of seasonal demand decline. However, as some steel mills are still profitable, it is expected that the overall decline in pig iron production will be relatively slow. Steel mills are exercising control over their raw material purchases, leading to an accumulation of coke inventories. On the coking coal front, most coal mines are maintaining normal production levels, with the daily number of vehicles passing through the Ganqimaodou port in Mongolia remaining at a moderately high level. On the demand side, with the second round of price cuts for coke initiated, market pessimism persists. Downstream buyers continue to restock on a need-basis. Online auctions at major mines are predominantly seeing price declines, with a high rate of unsold lots. Overall, although trade conflicts have eased, uncertainties remain significant, and market sentiment is cautious. April's macro data was weak. The fundamentals of coking coal and coke have further weakened, with coking coal expected to continue its downward trend and coke following suit. In terms of strategy, the bearish outlook persists.

Recommended reading:

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)